A Green Circle Capital White Paper

By Stu Strumwasser, Managing Director

Contributors:

Laura Mirro, Michael Mittiga and Greg Wank, Anchin (Accounting)

David Spungen, Corient (Wealth Management)

Kara Posner, Giannuzzi Lewendon (Law)

Yadim Medore, Pure Branding (Marketing)

Sean Conner, ForceBrands (Executive Recruiting)

June 2026 ©

Introduction

Preparing for an exit in order to maximize valuation and terms requires thoughtful long-term planning and execution, often over a period of one or two years, or more, prior to transacting. Green Circle Capital Advisors (and our colleagues who contributed to this white paper) work with growth-stage consumer brands. Green Circle helps them raise equity growth capital of between $5M–$25M and advises on M&A sale processes for brands with revenue typically between $10M–$100M.

We have observed a wide spectrum of preparation for an M&A sale process, from ill-conceived and disorganized, to perfectly executed like a military operation. In this high-level but comprehensive guide we provide recommendations from a financial perspective and draw on leading service providers across the CPG ecosystem to share insights from their respective areas of expertise. The goal is to aggregate a brief and impactful playbook of best practices to consider as one contemplates a potential exit in the near to intermediate term. Keeping this piece on hand as a reference may help growth-stage companies avoid a sub-optimal outcome and instead sprint powerfully toward a liquidity event.

I. Green Circle Capital Advisors: Finance and M&A

- We have returned to an EBITDA world. During the hot CPG market years of around 2014-2022 topline growth was more important than profitability or margin expansion—but that was an anomaly, and not the rule. Most businesses are valued as a multiple to a perceived future cashflow. It is common for young and high-growth brands (“high” as in 25%, 50% or even 100% YOY revenue growth) to be valued with a multiple to revenue. However, for brands over ten years old and/or not growing at those kinds of rapid rates…. Profits matter again. Today, a balanced approach showing strong growth and healthy EBITDA margin may make a business more attractive and valuable to acquirers. Strategizing on how to achieve that kind of financial performance can be augmented by the support of experienced advisors.

- Numbers don’t do deals; people do. When one is preparing to sell a business, executing the sale, managing a transition and guiding the business for a period of time post-transaction, the factors affecting those decisions are often driven by lifestyle choices for owners, not just financial ones. That said, a key financial consideration is this: founders don’t typically extract significant cash in minority deals. To do so usually requires yielding control in either a full buyout or the sale of a majority interest.

However, giving up control to de-risk and monetize doesn’t require selling one’s entire stake. Some CPG brand founders choose to sell a majority interest but stay on to partner with the new owners and continue to run the company while retaining a minority stake in the equity, often for three to five years. Once you have clarity on those lifestyle goals regarding whether to stay on, slow down, or leave entirely post-transaction, your advisors can help guide you to the right potential acquirers or partners and deal structure. - If one hopes to sell a brand in a couple of years, does it still make sense to suffer dilution in order to secure growth capital? The simplistic answer to this common question is that it depends. Robert Townsend, the former CEO of Avis and author of the influential business book Up the Organization, is credited with having said, “I’d rather have a small piece of a watermelon than a large piece of a grape.” The question is whether the current ownership stake would likely be worth more at the time of a sale than a smaller percentage might be worth—including the enhanced value created by that growth capital. While that may seem obvious, doing the actual math often seems to surprise people.

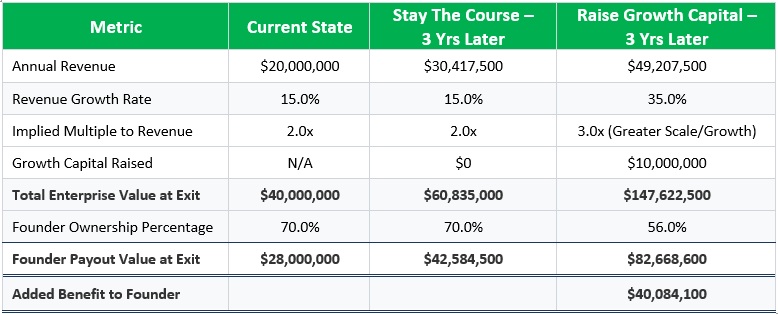

Let’s assume, for illustrative purposes, that a founder/owner owns 70% of a business, the brand is growing at 15%/year, generates $20M in revenue and the owner hopes to sell in two or three years. Let’s also assume, for argument’s sake, that the business is worth roughly two times revenue, or $40M. That would equate to the 70% stake being worth $28M. [We are not suggesting that is a fair valuation—it is merely an illustrative one. Valuation depends on numerous other factors such as margin profile, profitability, growth opportunities and drivers, product categories and competitive landscape, etc.] If that 70% owner didn’t want to incur dilution and stayed the course, in three years the business might grow to $30.4M in revenue and be worth $60.8M, meaning that 70% stake would have grown to $42.6M in value.

The idea behind raising growth capital, and perhaps also securing value-added partners in the transaction, is to accelerate growth, improve the business, and thereby increase the value. Hypothetically, if this $20M brand growing at 15%/year raised $10M in growth capital it might cause that 70% owner to incur 20% dilution, reducing their ownership stake to 56%. However… it might also enable the business to afford slotting fees, greater promotional and merchandising budgets, implement better systems, pay better vendors such as brokers/lawyers/marketing agencies/etc. and to staff up with additional executives, salespeople and marketing personnel. If doing so led to a growth rate of perhaps 35%/year, the business would grow to $49.2M in revenue in three years. With a greater growth rate and larger scale comes higher valuation multiples. If a $20M brand growing at 15%/year might be worth 2X revenue, then a roughly $49M brand with a 35% growth rate might be worth closer to 3X revenue. That would impute an enterprise value to the business of roughly $147.6M and a 56% stake in that business might be worth $82.7M, which is $40.1M more or nearly double what the owner’s stake might be worth had the owner not raised capital. The cherry on top of this financial sundae (a natural one of course, with no red dyes) is that the growth capital which might significantly improve the return for that owner might also reduce his/her risk, as the Company would be better capitalized, larger and more resilient, and have better resources and partners around the table.

Note: Green Circle has a proprietary “GC Dilution Matrix” we can share with growth-stage clients and prospective clients that can be used to illustrate such scenarios that are specific to your Company. The inputs are dynamic so one can change the growth rate, or multiples, or other assumptions and then see how that might affect various outcomes. Email stu@greencirclecap.com to request a free consultation and model.

4. Plan drivers for growth for the next owners (“meat on the bone.”) If launching new product lines or marketing programs with which to improve retail velocity and/or E-commerce KPIs, expanding into new distribution channels or foreign markets, etc. can be executed and show meaningful impact on growth rate and/or profitability within the 12–24 months prior to your desired exit, go for it. For those projects that may take longer to implement (or from which to benefit) it may very well make sense to wait. The reasons are twofold: the more uncertainty in the business at the time of a sale the more likely that some prospective buyers might pass or apply a discount for the assumed risk, and secondly, leaving those “meat on the bone” growth initiatives articulated-but-not-executed-upon creates a forward-looking growth story you can sell to the next owner, along with your current financial performance. Drivers for future growth opportunities are harder to quantify and may provide you with additional negotiating leverage.

II. Anchin (Accounting): Financial Reporting And Tax Readiness

For consumer brands considering an exit, success is the result of deliberate preparation over time. Today’s buyers are more selective; diligence is more rigorous; and valuation outcomes depend on confidence in a company’s financial and tax profile.

A lack of early planning often creates challenges in diligence that affect deal structure and tax efficiency—which could have been avoided in advance but are difficult to address once a process is underway. Companies that prioritize early preparation and build a more disciplined, decision-ready infrastructure to enhance financial sophistication, transparency in reporting, and operational processes tend to move through transactions more efficiently and achieve stronger outcomes.

1. Accounting & Financial Readiness.

A foundational step in preparing for an exit is strengthening financial reporting. Buyers usually expect GAAP-compliant statements that are consistent, transparent, and audit-ready. This includes proper treatment of complex areas such as revenue recognition, inventory costing, and equity-based compensation. Just as important, companies must clearly articulate their earnings story, with well-supported adjustments to present normalized EBITDA.

Visibility into profitability drivers is equally critical. Well-prepared companies can demonstrate performance at a granular level by SKU, customer, and channel, while providing insight into margin sustainability and trade spend effectiveness. This detail allows buyers to assess not only growth, but also the durability and quality of earnings. Disciplined working capital management, including clean receivables, supportable inventory balances, and normalized trends, can also reduce friction during negotiations.

Strong processes and internal controls help reinforce readiness. Companies that maintain reconciled accounts, documented policies, and consistent close procedures are better positioned to respond efficiently and credibly to diligence requests.

2. Tax Readiness & Planning.

Proactive tax planning can significantly improve after-tax outcomes and reduce execution risk. Priority areas include nexus analysis, state and local tax compliance, and sales and use tax obligations. Evaluating entity structure and potential benefits, such as Qualified Small Business Stock (QSBS), also unlocks meaningful value if addressed early.

A seller’s outcome depends on the headline price and net proceeds after tax. Many planning opportunities arise before deal terms are finalized. Conducting sell-side tax diligence in advance allows sellers to identify potential risks, quantify exposures, and assess the tax implications of alternative deal structures. This enables more informed negotiations based on expected net proceeds.

Early diligence also helps surface issues before buyers do. This reduces the likelihood of price adjustments or delays. Key workstreams include evaluating structure (asset vs. equity), modeling gains and losses, developing a purchase price allocation strategy, assessing deferral or exclusion regimes, and confirming entity-specific tax implications.

Advisors play an important role in guiding this process. Experienced advisors understand exit dynamics and can anticipate challenges, mitigate risks, and identify planning opportunities. Ultimately, exit readiness is about credibility. Companies with clean, supportable financials and a comprehensive tax strategy are more attractive to buyers. They are also better positioned to control the narrative, minimize surprises, and maximize value at closing.

By Laura Mirro, Michael Mittiga and Greg Wank

Contact: Greg Wank, Partner, Anchin, greg.wank@anchin.com

III. Corient (Wealth Management): Personal Wealth Transfer And Tax Mitigation

Given how consumed Founders tend to be while running a business they often don’t do sufficient pre-exit planning prior to heading into a sale process with respect to the transfer of wealth and mitigating tax consequences. While every owner’s situation is unique, the exercise tends to fall into 3 major categories:

- Optimizing for QSBS treatment. Many startups meet the criteria for QSBS qualification, which affords them the ability to not be taxed on sale proceeds of $10M or $15M (depending on when their C-Corp was formed) or possibly more if they converted from an LLC when it had basis. If the expected proceeds are likely to exceed that amount, thoughtful trust planning can provide additional taxpayers to “stack” the exemption (the amounts are per taxpayer). The planning around this is somewhat complex and should be executed thoughtfully, and so should be done well in advance of an actual transaction.

- Pre-transaction transfers of equity to mitigate potential estate taxes. In many cases, Founders’ estates exceed the lifetime gift and estate tax exemptions (currently $15M per individual, $30M per couple), which could subject their heirs to a 45% marginal tax rate on the net value of their estates. By transferring a portion of the equity in their companies prior to signing an LOI for a sale, they can move substantial assets out of their estates at a lower valuation than the transaction value, including possible discounts allowed for lack of marketability and minority ownership. Doing so could potentially minimize or even eliminate the estate tax that would otherwise be due at the second of their and their spouse’s deaths.

- Gifts of Business Interest to a Donor Advised Fund (DAF). If a Founder is charitably inclined, they can create a pool of assets for philanthropic purposes in a tax-efficient manner by contributing a portion of their equity in their business to a Donor Advised Fund (DAF). That excludes the amount gifted from tax at the sale, and provides an additional charitable tax deduction.

Making these important financial decisions amid the pressure of closing a major transaction is not ideal. Proper planning should begin in earnest when a Founder raises an A or B round and a substantial valuation that results in their equity prospectively being worth $10M or more. Determining priorities across lifestyle, support for extended family, philanthropy, a potential new business, etc. can inform what planning levers they want to pull and to what degree.

Contact: David Spungen, Partner & Managing Director, Corient, David.spungen@corient.com

IV. Giannuzzi Lewendon (Law): Common Diligence Pitfalls That Delay, Devalue, or Kill CPG Transactions

As corporate counsel representing consumer brands through financings, acquisitions, and other liquidity events, we routinely see diligence findings materially impact valuation, deal structure and timing, and, in some cases, kill deals altogether. Below is a brief recap of some of the important issues that often come up, and which business owners can usually address in advance of a sale.

- Capitalization. Buyers want a clear and defensible record of who owns the company, and how that ownership came about. Every issuance, transfer, repurchase, forfeiture, option grant, SAFE conversion, and other equity-related event should be properly documented and traceable from inception through closing. Missing board approvals, inconsistent cap tables, or undocumented shifts in ownership can create tax and other legal issues and cast doubt on the sellers’ ability to deliver clean title to the equity being sold.

- Ownership of Intellectual Property. In the consumer products world, relatively few intellectual property assets can be evidenced through filings or registrations (like trademarks). Founders often assume that because they paid for a logo or formula, the company owns it, but that’s not always the case. Buyers often focus on what we call the “web of contracts” surrounding the business to confirm they are buying the entire asset. They will expect to see written confirmation that every founder, employee, consultant, agency, manufacturer, research partner, and other contributor has properly assigned any relevant intellectual property rights to the company.

- Product Labeling and Claims. Product labeling and marketing claims have become an increasingly important diligence focus and, when significant issues are identified, are often the most likely concern to cause a buyer to walk away. Statements regarding functionality, efficacy, health benefits, sustainability, ingredient sourcing, or product performance should be supportable and compliant with applicable regulations. Issues in this area can create regulatory and litigation exposure post-closing, as a publicized acquisition can transform an otherwise overlooked brand into an attractive target for plaintiffs’ firms looking for labeling and claims-related violations.

- Commercial Contracts. Commercial contracts often contain provisions that become highly relevant in an acquisition context. Manufacturers, distributors and other key service providers may have notice, consent, termination, or other change-of-control rights that can slow down or complicate deal execution. We have seen seemingly innocuous provisions buried within boilerplate language create outsized leverage for third parties during a transaction, resulting in sellers paying substantial sums simply to obtain a signature that should never have been required in the first place. Assessing these issues in advance can help save critical time and money later.

For brands we meet early in their life cycle, we help establish best practices on these (and all other) fronts from day one. For brands we meet later, we often conduct a mock buyer diligence review to identify and remediate issues before a sale process begins. Proactively addressing potential roadblocks helps avoid surprises, preserve negotiating leverage, and maximize transaction value.

Contact: Kara Posner, Partner, Giannuzzi Lewendon, kara@gllaw.us

V. Pure Branding (Marketing): Protecting The Intangible Layer of Brand Value

For more than twenty years, Pure Branding has supported natural CPG brands. Our traditional focus on the supplement and nutrition category has given us an up-close and unique view into a category where science, claims, efficacy, and consumer belief collide every day. Those attributes have become more important and relevant in adjacent categories of health & wellness including food, beverages, etc., where many are entering the same maturity cycle supplements entered years ago: better ingredients and rational claims alone are no longer enough to create durable preference.

The brands that break away often build something deeper: belief. By belief, we mean more than trust. Consumers increasingly choose brands based on philosophy, standards, worldview, sourcing, founder credibility, transparency, and emotional alignment. They want to feel that a brand reflects how they think about health, wellness, and quality of life. Leveraging those best practices and applying the lessons learned to all consumable brands can add critical value in sharpening and preparing a brand for a sale process.

The supplement industry became highly sophisticated at feature-benefit marketing but over time many brands discovered that functional differentiation alone could not sustain pricing power or long-term loyalty because competitors could often make similar claims with similar evidence.

Growth also often introduces subtle forms of brand erosion long before performance weakens financially. Expansion across channels, new product launches, retailer pressure, investor expectations, and operational scaling can slowly dilute the very qualities that created emotional connection in the first place. For founders preparing for acquisition, this creates an important challenge. The diligence performed during a sale process can shine a light on such weakness.

For founders and owners preparing to sell a brand, assessing brand strength often depends more on psychographic connections than on demographics. First, assess whether loyalty is psychographic rather than product-driven. Many leadership teams believe customers are attached primarily to ingredients, formulations, or product superiority when loyalty may actually be tied to worldview, aspiration, trust cues, or emotional alignment surrounding the brand.

Second, assess whether the brand story has fragmented during growth and update it as needed. As companies scale, messaging often becomes inconsistent across packaging, digital, retail, Amazon, social media, and innovation. Sophisticated buyers notice when a brand no longer feels coherent.

Third, identify what should not be standardized. Founder voice, hero products, sourcing philosophy, practitioner credibility, or community trust may carry far more symbolic weight with consumers than internal teams realize.

Finally, make that belief system legible to buyers. Founders should be prepared to demonstrate how emotional equity supports pricing power, repeat purchase, channel expansion, and resilience after the business changes hands.

Buyers may not always name belief as a diligence item, but they are looking for evidence that loyalty will endure beyond the founder, the current team, or the current growth curve. The most compelling natural CPG brands are those that can demonstrate not only how the business scales, but why consumers will continue to care as it does.

That is often the value buyers are truly acquiring.

Contact: Yadim Medore, Founder and CEO of Pure Branding, yadim@purebranding.com

VI. ForceBrands (Executive Recruiting): Building the Team Before You Need It

For nearly two decades, ForceBrands has helped high-growth consumer brands and their investors make the leadership decisions that shape their next stage. We align each brand’s people strategy to the growth plan, so the team is built for where the brand is going, not where it has been.

The constant in a changing market

Trends shift. Categories evolve. Challenger brands disrupt overnight. But one constant holds across every high-growth brand we have worked with: the businesses that win — and transact well — are built on exceptional leadership teams, supported by boards that know how to guide them.

The most consequential mistake founders and PE-backed CEOs make is not a missed product or channel decision. It is failing to build the right organizational structure ahead of the growth already underway. By the time an exit is announced, most are reacting to a leadership gap rather than executing a plan they built in advance.

The 12-to-24-month blind spot

Our research shows that 60% of executives are open to or planning a transition within the next year, and most of those decisions are already forming before the company notices. At the same time, 66% of executives say there is no succession or backfill plan for their role, and 48% of CEOs have no succession plan in place for their top three positions.

This is the blind spot. Our data supports the idea that founders and investors often treat leadership planning as reactive: a search that begins when a seat is empty. The best organizations treat it as a forward discipline, no different from financial planning or capital allocation.

Structure follows growth — until it doesn’t

In high-growth consumer brands, structure rarely keeps pace with scale. 70% of executives say their role has evolved without corresponding updates to structure. Nearly 20% say their position should be restructured if they were to leave.

A business ready to thrive after a leadership exit does not depend on any single person. It has the right leaders in the right seats, with clear scope and authority to execute — and that structure is built deliberately, 12 to 24 months before it is needed.

The audit every CEO and Board should run now

The single most valuable action a founder or PE-backed CEO can take in the 12-to-24-month window is an honest organizational audit. Does the structure reflect the business today? Are the right leaders in the right seats, retained with the right incentives, and backed by a board equipped to guide — not just oversee — a transition? The answers determine whether the organization is ready.

Data references: ForceBrands 2026 C-suite Salaries & Executive Sentiment Report, based on two surveys of consumer brand C-suite leaders and EVPs conducted in April and September 2025.

Contact: Sean Conner, Co-Founder & Managing Partner, ForceBrands, sean@forcebrands.com

Contact Information:

Stu Strumwasser, Founder & Managing Director, Green Circle Capital Advisors (Investment Banking)

stu@greencirclecap.com

Contributors:

Greg Wank, Partner, Anchin (Accounting)

David Spungen, Partner & Managing Director, Corient (Wealth Management)

Kara Posner, Partner, Giannuzzi Lewendon (Law)

Yadim Medore, Founder & CEO, Pure Branding (Marketing)

yadim@purebranding.com

Sean Conner, Co-Founder & Managing Partner, ForceBrands (Executive Recruiting)

If you would like to send this whitepaper to a CEO or other friend, please enter the brief information below:

This document is the property of Green Circle Capital Partners LLC and for information only. It is not an offering for sale of any securities. The financial estimates and projections contained herein are purely hypothetical and in no way representative of any investment opportunity or guaranteed for accuracy. This document may not be distributed or reproduced without the express written permission of Green Circle Capital Partners LLC, New York, NY. © 2026

Registered Representative of and Securities Products offered through BA Securities, LLC. Member FINRA & SIPC. Green Circle Capital Partners LLC and BA Securities, LLC are separate, unaffiliated entities.